CPC(TDS) Advisory for Deposit of Tax deducted and Demand for TDS Defaults with respect to Purchase of Immovable Property (26QB Statement-cum-challan)

The Centralized Processing Cell (TDS) provides important tips, for the convenience of Taxpayers, who have executed any transaction for Purchase of Immovable Property exceeding Rs. 50 Lakhs (Rupees Fifty Lakhs). Please take note of the following key details for Payments associated with filing of 26QB Statements-cum-challan and TDS Defaults, if any:

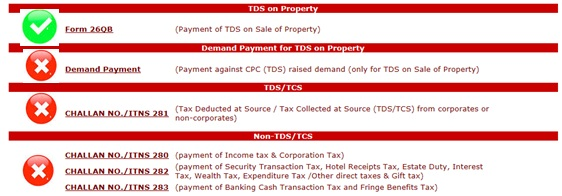

Filing of 26QB Statement-cum-Challan:

1. 26QB Statement-cum-challan can be filed (along with payment of tax), under “Form 26QB” in “TDS on Sale of Property”on the payment portal of NSDL.

2. The tax to be deposited only through the Statement-cum-Challan mode (Form 26QB). No other challan, viz. Demand Payment, 280/ 281 etc. to be used for the same.

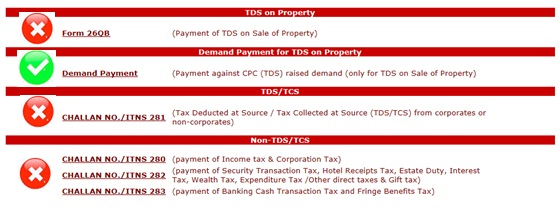

Payment against TDS Defaults:

1. On receipt of Default Intimations from CPC(TDS), the Payment against demand raised should be made through the Demand Payment link at NSDL portal, as follows:

2. The payment of Demand for closure of Defaults has to be made only through the above online mode. No other challan, viz. 280/ 281 etc. should be used for payment of demand.

CPC (TDS) is committed to provide best possible services to you.

CPC (TDS) TEAM

AO is under an obligation to duly consider the explanation furnished by the assessee and assign reasons for rejecting the…

CBIC issues SoP for clearance of imported goods through Foreign Post Offices under Postal Import Regulations, 2025. Standard Operating Procedure…

Sale deed executed with full knowledge of only part consideration paid, cannot be rendered void or inoperative merely for non…

No fault in serving notice u/s 148 to last known address when assessee had not updated change of address in…

Investment made by firm through capital introduced by partners cannot be treated as unexplained investment in the hands of the…

Multipurpose Empanelment Form (MEF)- 2026-27 is hosted - Last date for submission is 29.08.2026 ICAI has hosted the Multipurpose Empanelment…

{kind=link}

{kind=link}