ABCAUS Excel Depreciation Calculator FY 2022-23 under Companies Act 2013 as per Schedule-II Version 04.26

The maiden ABCAUS Excel Companies Act 2013 Depreciation Calculator was first launched in March, 2015.

The ABCAUS Depreciation calculator for FY 2022-23 has also been formulated and styled the same way as its predecessor so that users find themselves familiar with it.

This calculator is meant for companies following April to March Financial year. Also the calculator is meant only for tangible assets. Like, in last year useful life of the assets purchased during the FY 2022-23 is taken in integers only.

Any error or suggestions may please be reported at lohni@yahoo.com

ABCAUS Excel Depreciation Calculator FY 2022-23 under Companies Act 2013

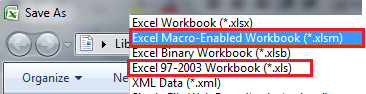

Saving the file to your local computer disk

Please note that while downloading this utility save it as either Excel 97-2003 (xls) or Macro Enabled sheet in Excel 2007 or later versions (.xlsm) Only

How to use this calculator?

The calculator has been divided into five part as under:

(a) Assets

(b) Opening Details

(c) Additions

(d) Opening Deletions, and

(e) Depreciation Chart

In each part only “grey” fields are required to be filled.

Assets

Assets database should be created by providing names of the assets and by selecting the asset type as per schedule-II. Please note that no two names should be identical. If for example there are multiple computers, they should be written in different rows as computer1, computer2…and so on.

Since, you must be having the individual asset-wise list of closing wdv as on 31/03/2021 or the depreciated value of the asset as on 31/03/2014 (for SLM purposes) creating this database should not be a problem.

Please note that new assets purchased during FY 2022-23 should also be filled in this database. Again, please bear in mind that they should also be unique and not bear an identical name to an existing asset.

For example:

You have opening wdv of the block furniture individually for each asset (say, “furniture1”, “furniture2”, “furniture3”) and if during FY 2022-23 there is another addition to the block furniture, then a new nomenclature (say, “furniture4”) should be used in the asset sheet. In the “new addition sheet” this new furniture “Furniture4” is required to be selected for calculating depreciation on new additions.

Opening Balances:

Since the users must be having individual asset wise closing wdv as on 31/03/2022, the details required in the opening sheet should be filled using the wdv list as on 31/03/2022.

For SLM purposes, depreciated book value of the assets should be filled in column B.

In the Opening WorkSheet, the following particulars are required to be given:

- Name of assets > fill the “Asset Sheet” as per closing wdv list of FY 2021-22 and select by drop down

- Depreciated value of asset as on 01/04/2014 (if using SLM)

- WDV as on 01-04-2022 > as per closing wdv list of FY 2021-22. If useful life of the asset was zero as on 01/04/2014 it would be equal to the residual value.

- Remaining useful life > as per useful life as on 01/04/2014 minus three years

- If useful life zero as on 01/04/2014 > Select Yes or No

- If asset has been sold during FY 2022-23 > select Yes or No from drop down

- Estimated residual value > as estimated during FY 2014-15. By default it was taken 5%

- Depreciation Rate > The rate as calculated in FY 2014-15 should be filled

- Rest of the values shall be calculated automatically

- Date of format should be dd/mm/yyyy

- No field should be left blank.

Additions made during the year

- Date of format should be dd/mm/yyyy

- For each new additions, first they should be created in ‘Assets” sheet.

- For new additions made during the year, residual value has been taken @ 5% by default.

- If any disposal has been made out of additions during the year, its details must be filled in columns ‘f” and “g” after selecting “Yes” in column “e”

- Please note that useful lives of assets can be altered from the sheet useful life.

Opening-Deletion

- This sheet accounts for any deletion that has been made out of the opening assets, (i.e.; out of opening sheet)

- Only those assets which have been disposed off during FY 2022-23 should be selected under assets name list.

- If you have selected “yes” against any asset in column “f” in opening sheet, the same asset must be selected here

- Date of format should be dd/mm/yyyy

- Date of purchase of disposed asset should be available as per depreciation chart prepared for FY 2014-15.

- This sheet must be filled after completing the ‘Opening sheet”

Depreciation Chart

It should be automatically calculated.

See Video Tutorial:

The calculator is meant to guide and help in calculating the depreciation, the disclosure requirements have to be separately taken care of.

Also the WDV written off should be charged either to reserves and surplus or profit and loss account.

Similarly, Profit or loss on the disposal of assets should be reflected in profit and loss account.

ABCAUS Excel Depreciation Calculator FY 2022-23 under Companies Act 2013

Please note that by downloading the ABCAUS depreciation calculator, you agree to the terms of use that you do not have permission to modify, copy, edit, upload, reproduce, republish, distribute or transmit the utility except with the written prior approval.

Depreciation Calculators for preceding years are as under:

| FY 2021-22 | Click Here to download |

| FY 2020-21 | Click Here to download |

| FY 2019-20 | Click Here to download |

| FY 2018-19 | Click Here to download |

| FY 2017-18 | Click Here to download |

| FY 2016-17 | Click Here to download |

![]()

- Commonality of directors of companies does not mean deposits received was bogus

- Application though named as rectification but if tax is not legitimate, it also touches merit: HC

- Cost of acquisition as on 01.04.1981 taken as per valuer report by reverse indexing of FMV

- AO was directed to serve notice of hearing through physical mode upon assessee

- ICAI Intermediate & Foundation Examinations to be held thrice in a year from May/June 2024

{kind=link}

Sir, When depreciation calculator for AY.2024-25 WILL BE READY

SIR

WAITING FOR DEPRECIATION CALCULATOR AY 2023-24

Thanks for this depreciation utility which I am using from the beginning i.e 2015. I wish you all the best in your new creations. Good work.. Make life easy in busy schedules… Thanks once again

Sir, I have downloaded cos act depreciation calculator 2018-19,

while calculating in ‘Additions’ sheet, it is showing negative figures in dep for year 2018-19.

Depreciation is wrongly added back to the purchase cost and it is showing wrong figures.

Please help for the same.

Thank You.

download revised version 7.10

waiting for depreciation calculator for A/Y. 2019-20. when it will be ready sir?, as we have to prepare Balance Sheet.

Waiting for depreciation calculator for F Y 2018- 19 (A.Y. 2019-20). When it will be ready Sir?,

waiting for depreciation calculator for A/Y. 2019-20. when it will be ready sir?, as we have to prepare Balance Sheet.

by 1st week of May 2019

I am not getting link of downloading the excel

There is no link to download the file. Can you please provide it.

Waiting for depreciation calculator F.Y.2017-18. When we can download sir?

just released

When will we get depreciation calculator for f.y. 2017-18 ?

expected within the 1st week of June

Dear Sir,

Please provide immediately Depreciation chart ( abcaus Excel Depreciation Calculator FY 2017-18 Companies Act 2013)

Dear Sir,

Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz Plz provide immediately Depreciation chart ( abcaus Excel Depreciation Calculator FY 2017-18 Companies Act 2013)

I am afraid that you will have to wait till next month

Dear Sir,

Please Sir provide immediately Depreciation chart ( abcaus Excel Depreciation Calculator FY 2017-18 Companies Act 2013)

just released

Sir,

Please provide abacus Excel Depreciation Calculator for FY 2017-18 Companies Act 2013.

Dear sir,

Request you to provide abacus Excel Depreciation Calculator for FY 2017-18 Companies Act 2013.

Thanks for providing your previous years abacus depreciation calculators.

Regards,

vihang

Dear Sir

Please send the password of old files which i mailed you yesterday.

Thanks

Dear Sir

I downloaded the depreciation calculator in 2016 and used the same for calculating 2016 , but unfortunately lost the password , now how i get the password,can I send the file .

The sheet for calculation of derpreciation is password protected, please send me the password. thanks

I have sent mail but still I am not received the link & password for excel depreciation calculator for the FY-2016-17

Thanks

Jayakumar

How to activated the link . I have already subscribed the link.

downloading option is not available or please send me link for download

Dear Sir,

We find that, we do not have the xls sheet for computing the depreciation for 2016-17. What is the update of the same ? Can you please help us to have the same

Regards

CA J Mohan

pls wait till the end of the month

depreciation calculator for FY 2016-17 provided ?

sorry.

no such request received with this email id.

Admin

Sir

Please provide the excel depreciation utility for FY 2017-18.

Sir Thank you for the password. Is there any changes / modification for in depreciation calculator after the version 1.50. please let me know sir

Delivery to the following recipient failed permanently.

I have not yet received any password

Dear Sir,

I have complied with the said procedure and haven’t received the password yet.

no such email received

I HAVE NOT RECEIVED PASSWORD YET

No password received yet, if it is freeware why so much of delay in sending password, can we really get the password or not, let us know asap, if not we can find few alternative calculators

Attention: You are advised to adhere to the steps suggested for getting password.

Still i m not received utility passw0rd . can you send me again .

When we have sent you the details for password, we are getting the error mail saying the below…

Delivery to the following recipient failed permanently:

info@abacus.in

Technical details of permanent failure:

The recipient server did not accept out requests to connect.

Please send us the alternate method to get the activation password

retry

Sir

I have not received, once again please send it

Sir I have requested for password for Abcaus Excel depreciation calculator for 2015-16. So far I have not received. sir I have already subscribed to your website

Password has been sent to you. Check your spam/junk folders.

I have Sent the 3 times mail for Password, but still not get password or any respond. so without password this is no use the excel sheet

Rajesh

You were sent password two times. check your junk or spam folders. Users are advised to add info@abcaus.in to their email address book so that password/response do not land in those folders.

I am getting updates from you regularly but password to open depreciation calculator is not yet received while i had followed all the steps to get password, so Please send me the password, as earliest

We have not received any compliance on your part as per required guidelines. In many cases emails were sent to wrong address, users did not subscribe or furnish short/incomplete details.

In fact all users are advised to go through the guidelines carefully.

Admin

We have subscribed to the news letters from Abacus, and sent you the required details for password. We have not received any Password. Please send us the Password

NOT RECEIVED THE PASSWORD

Depreciation chart is password protected ..i have click on the link sent by you but still no information has been required by you regarding name address etc.

Kindly observe the required guidelines carefully.

Please everyone.

Observe the requirements for getting a password carefully. emails with incomplete or short details are not replied

Kindly provide Password for Utility so that we can compute Depriciation queekly.. we registered our email ID & provided the details as per requirement.

Thanks

CA Bhadresh Sanghavi

Kindly enable a system for quick generation of passwords so that it would be useful at the right time. Thank you in advance,

CA K V Venkitaraman.

Cannot activate the subscription by clicking on the Link as error coming as ” class not registered”..pls reply how else to get the Depreciation Calculator for 2015-16 as it is very user friendly ..used it last year

Sir I have followed the steps as instructed by you, kindly send me the password.

Regards

shivachandraca@gmail.com

dear sir

im not able to open calculator pls provide password

I HAVE ACTIVATED EMAIL AND DOWN LOAD THE EXCEL SHEET BUT I DONT HAVE PASSWORD PLEASE SEND THE PASSWROD

Dear Sir, Provide me password for excel depreciation computation..

i did not get password after all the activation of news letters in order to open the depreciation sheet

As said earlier, pls observe the required steps for getting the password.

Dear Sir,

Thanks for calculation sheet.

Could you please tell us the steps involved in depreciation calculation.

Please read help file thoroughly and see video tutorial.

I Have Not Recd the Password to open excel sheet

kindly provide us

Thanks

Shubham

I have not yet received password for activation of excel sheet after 3 days of activation.please give the password

Dear Sir,

In your download option version 1.00 is being shown not 1.50

Please send 1.50

Thanks

that was just a typo error , corrected now

Hi Dear,

I couldn’t get any password yet.

pls sent me it asap

Thanks

Dear Sir,

Refers to my several reminder i am not getting password of your excel base depreciation sheet even i am getting your various mails.

thanks,

sanjeev shukla

reachsshukla@gmail.com

Password not yet received after 1 day of subscription

The password is not received yet. Kindly send the same at the earliest.

PASSWORD NOT RECEIVED YET

Dear Sir

I had not received the password till yet pls send the password to open the depreciation file

I have not received the password yet. It is a bit disappointing sir.I request you to kindly send me the password .

Everybody!

Please make sure that you adhere to the requirements for getting a password. It has been observed that considerable email are received without the proper information as required.

NO PASSWORD YET

please provide me the password to open the calculator

I am download Abacus companies act depreciation F.Y.2015-16. but file is password protected.

how to find the password.

I HAVE NOT RECEIVED THE UTILITY PASSWORD YET .

Password for your excel is not received yet. Request you to send

Vishal

Dear Sir,

Please arrange to provide the password of your excel based depreciation calculator for 2015-16

thanks,

sanjeev shukla

We have not received the password after 3 days of activation

Kindly do the needful

thanks

jayakumar

Please not carefully;

To get password, the following is required:

1. Subscribe to newsletter and activate the subscription

2. apply for password at info@abcaus.in (and not at any other email)

3. write your name, address and contact number

Sir i did all but still am not received password kindly send that because time is going so i need that

As per the instruction given in the word document i have subscribed two days ago however no password has come to my mail id and i have even checked the spam folder too. Can u please send it again

Dear sir

pl. send the password

rgds

Nilesh Vyas

Dear Sir

Please give me Password of excel so that i am able to open Depreciation Calculation Excel sheet

Not reading carefully, the instructions to get a password could be the only reason if you have not received the password yet.

Dear Sir

i have subscribe of this site so please give me password of excel sheet

Dear sir

Pls send password to open xls. i have subscribed already

I have not received the password for depreciation calculator as per companies act for the FY 2015-16 even in spam & junk also it is not received. pl send the password at earliest

Dear Sir,

I have gone through your instruction ,i have even checked my junk n spam box but did not find any mail… plz suggest what to do. or send me password on mail. –

Pls note the instructions for getting the password carefully.

Please send me the Password for Excel Depreciation Calculator 2015-16 under Companies Act 2013, Schedule-II V

I just subscribe to your website, but did’t got the password to use the utility for calculation of depreciation. I even has registered myself with your website with my email id But no password is sent to me

Please send me the password

Dear Sir,

I subscribed to your website last one week, but didnot got the password to use the utility for calculation of Depreciation, please send password.

Thanks,

Parankush Tiwari

Please send me the Password for Excel Depreciation Calculator 2015-16 under Companies Act 2013, Schedule-II V-1.10

Thanks

The password has again been sent to you.

Make sure that after subscribing to newsletter, it is also activated by clicking on the activation link send to your email. (see also in junk or spam folders). Also keep in mind that sending of password might take 2-4 hours. In case you have not received password email, check your junk or spam folders.

i even checked junk n spam box but did not find any mail… plz suggest what to do. or send me password on mail. thanks

i have not yet received password for depreciation utility after subscribing for email & sending mail on info@abcaus.in…

Awaiting response

How to know our pass word .kindly do the needful.

Sir,

Accounting year 01/04/2017 to 31/03/2018 calculator have you public ?

how to know.

thanking you.

check updates

I used the Password supplied but it not opens the file.

Is this a free download or paid download., the Sheet is password protected ., if I request for password ., I am not getting it

Dear Aarthi, It is absolutely a free utility. Password is sent asap within 24 hours.

thanks

if you don’t wish to provide the password then no need of a excel sheet as i have tried several time send a mail but after one subscription i m still waiting for the password……………….

we are not finding the download link of excel file depreciation of abcaus

Firstly i am not getting the like to download abacus dep calculator for fy 15-16 on your website