Comptroller and Auditor General (C&AG) Report No. 03 of 2016 for the year ended March 2015 on Compliance Audit on Direct Tax Department Union Government tabled on 11-03-2016.

As per the report the instances mentioned are those which came to notice in the course of test audit for the period 2014-15 as well as those which came to notice in earlier years but could not be reported in the previous Audit Reports; instances relating to the period subsequent to 2014-15 have also been included, wherever necessary.

Chapter V: Transfer Pricing

5.1 Introduction

Transfer Pricing (TP) refers to the pricing of cross-border transactions between two related entities. When two related entities enter into any cross-border transaction, the price at which they undertake their transaction is called Transfer Price. Due to the special relationship between related companies, the Transfer Price may be different than the price that would have been agreed between the unrelated companies. Price between unrelated parties in uncontrolled conditions is known as the “Arm’s Length Price (ALP)”. Transfer prices thus serve to determine the income of parties involved in the cross-border transactions.

The Finance Act, 2001 introduced Transfer Pricing Regulations, the provision of which has been incorporated into the Income Tax Act, 1961 (Act) by enacting sections 92 to 92F in substitution of the erstwhile Section 92 of the Act. The Rules 10A, 10B, 10C, 10D and 10E of the Income Tax Rules, 1962 (Rules) complementing the TP Regulations have also been inserted in the Rules. These provisions deal with computation of income arising from “international transactions” with “Associated Enterprises (AEs)” or Specified Domestic Transactions. The regulations provide that any income arising from an international transaction shall be computed having regard to the ALP.

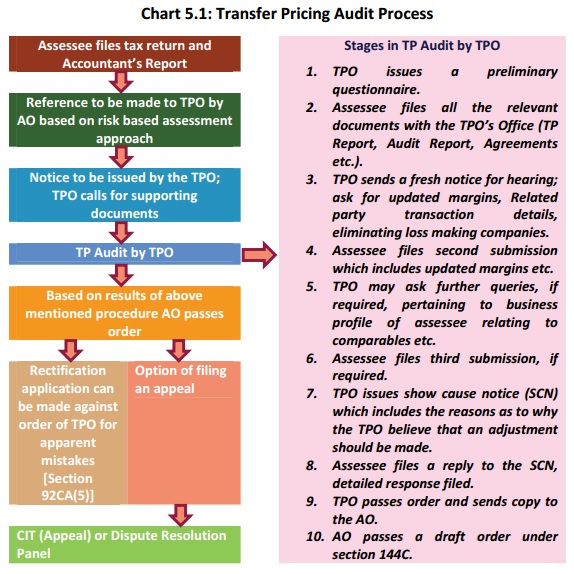

The procedure adopted by ITD as per the Act and CBDT’s instruction issued from time to time is detailed in Box 5.1.

| Box 5.1: Provisions of Transfer Pricing |

|

The computation of ALP under section 92C should be referred to the Transfer Pricing Officer (TPO). The TPO, after hearing the assessee, the evidence produced by him and after considering the evidence as required on any specified points and after taking into account all relevant materials which he has gathered, shall by order in writing determine the ALP in relation to the international transaction in accordance with provisions of section 92CA(3) and send a copy of his order to the Assessing Officer (AO) and to the assessee for finalization of assessment order. Section 92C(2) provides that the variation between the ALP and price at which the international transaction has actually been undertaken does not exceed five per cent of the latter, the price at which the international transaction has actually been under taken shall be deemed to be the ALP. Under section 144C(5), the Dispute Resolution Panel (DRP) shall issue the directions, as it thinks fit, for the guidance of the AO to enable him to complete the assessment after considering report of TPO. Section 92D(1) provides that every person who has entered into an international transactions shall keep and maintain such information and documents as may be prescribed in Rule 10D of Income Tax Rules. Further under section 92E, the person who entered into an international transaction shall obtain a report from an accountant in prescribed Form 3CEB showing all details relevant to international transactions. |

Chart 5.1 shows Transfer Pricing Audit process and various stages as adopted by the ITD.

5.2 Dispute Resolution Panel

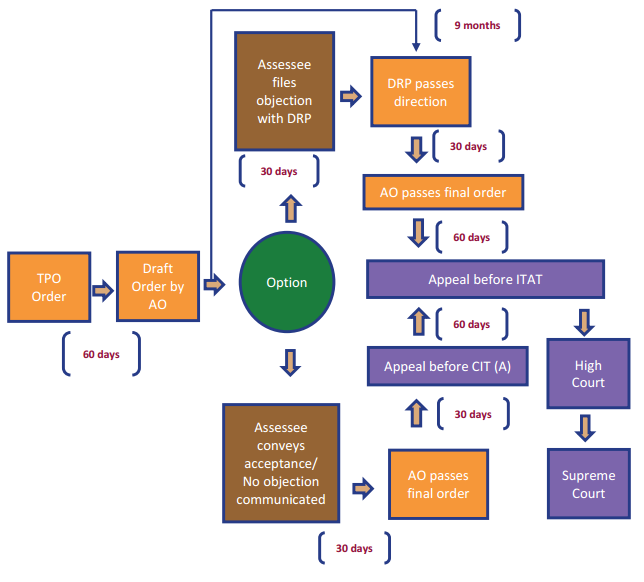

In order to streamline the process of redressal of disputes, the Finance Act, 2009 introduced the concept of a Dispute Resolution Panel (DRP) to provide for an alternate dispute resolution mechanism which would facilitate expeditious resolution of disputes relating to Transfer Pricing in International Transactions. Section 144C governs the provisions relating to DRP and subsection 15 of section 144C defines DRP as a collegium comprising of three Principal Commissioners or Commissioners of Income Tax (CsIT) constituted by CBDT for this purpose. In exercise of the powers conferred by sub-section (14) of section 144C, CBDT may make rules for the purposes of the efficient functioning of the DRP and expeditious disposal of the objection filed under sub-section (2) by the eligible assessee.

Chart 5.2 shows Dispute Resolution Process as available to the Assessee under the Act.

Chart 5.2: Process of redressal of disputes

5.3 Audit findings on Transfer Pricing Orders

We selected TP orders passed during January 2014 to January 2015 by TPOs of Ahmedabad, Hyderabad and Mumbai. We give below 10 high value cases where TPOs made mistakes in arriving at ALP and adjustments thereof.

5.3.1 In Maharashtra, CIT (TP)-3 Mumbai Charge, TPO passed the order of the assessee company (Reliance Mediaworks Limited) under section 92CA(3) for AY 2011-12 in November 2014 at an adjustment of ` 30.63 crore on the international transactions of corporate guarantee and interest recoverable from Associated Enterprises (AEs) on loan advanced to them.

Audit scrutiny revealed that the TPO, in his order, proposed interest to be charged at the rate of 12.69 per cent on the outstanding/fresh loans given to its subsidiary company RMW USA Inc in order to determine the ALP of transaction. However, TPO did not compute interest on outstanding loan of ` 18.18 crore, resulting in short adjustment of an equal amount. Further, while computing the interest on the outstanding/fresh loan given to UK share holding company, total interest amount was added at ` 3.79 crore instead of ` 3.91 crore, resulting in short adjustment of ` 0.12 crore. The above mistakes resulted in total short adjustments of ` 18.30 crore. The Ministry accepted (December 2015) and has taken remedial action under section 92CA(5) read with section 154 in November 2015.

5.3.2 In Maharashtra, CIT (TP)-4 Mumbai charge, TPO passed the order of the assessee company (Vedanta Aluminum Limited) under section 92CA(3) for AY 2011-12 in January 2015 at an adjustment of ` 2.30 crore in respect of interest on loan paid to AE. Audit scrutiny revealed that the assessee entered into an External Commercial Borrowing (ECB) loan agreement with its AE (Welter Trading Limited, Cyprus) for a loan in Japanese Yen (equivalent to US $ 400 million). As the term of loan was more than five years, the maximum all in costs ceiling as per Reserve Bank of India (RBI) Circular53 was six months LIBOR +500 basis points. However, TPO while calculating Arm’s length interest paid to AE, took 12 months JPY LIBOR interest rate+ 500 bps against the six months JPY LIBOR interest rate+ 500bps. Thus, maximum interest rate payable was worked out at 5.659 per cent54 instead of 5.431 per cent. The mistake resulted in incorrect computation of “Arm’s length interest ought to have been paid” at ` 30.26 crore instead of ` 29.04 crore leading to short adjustment of ` 1.22 crore. Further, the assessee entered into another ECB loan agreement with its AE (Welter Trading Limited, Cyprus) for a loan of US $ 500 million having term of loan for more than five years. TPO considered interest rate payable as 5.923 per cent55and made no adjustment as the transaction between the assessee (paying interest rate at 5.9 per cent) and AE was at Arm’s Length. Audit scrutiny revealed that TPO erroneously considered interest rate payable as 5.923 per cent instead of 5.519 per cent by taking 12 months US $ LIBOR interest rate+ 500 bps against six months LIBOR interest rate+ 500 bps which resulted in short adjustment of ` 8.68 crore on account of excess interest paid by the assessee to its AE. These mistakes resulted in short adjustment of ` 9.90 crore. The Ministry accepted (December 2015) and has taken remedial action under section 92CA(5) read with section 154 in November 2015.

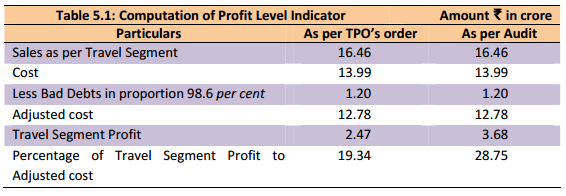

5.3.3 In Maharashtra, CIT (TP)-4 Mumbai charge, TPO passed the order of the assessee company (Thomas Cook India Limited) under section 92CA(3) for AY 2011-12 in January 2015 at an adjustment of ` 17.56 crore. Audit scrutiny revealed that TPO recalculated Profit Level Indicator (PLI)56 of the comparable of Trade Wings Limited for Travel segment level and arrived the adjusted cost after reducing the bad debts, however, PLI of comparable was computed at 19.34 per cent instead of 28.75 per cent as details given in table 5.1 below.

Thus, incorrect calculation of PLI of comparables resulted in short adjustment of ` 3.52 crore. The Ministry accepted (December 2015) and has taken remedial action under section 154 in June 2015.

5.3.4 In Maharashtra, CIT (TP)-1 Mumbai charge, TPO passed the order of the assessee company (Aditya Birla Minacs Worldwide Limited) under section 92CA(3) for AY 2011-12 in January 2015 at an adjustment of Rs. 13.25 crore. Audit scrutiny revealed that TPO, while calculating adjustment on account of interest on loan given to AE, adopted 22 days instead of 68 days for a loan period from 14 January 2011 to 22 March 2011. The mistake resulted in short adjustment of Rs. 52.59 lakh. The Ministry accepted (December 2015) and has taken remedial action under section 92CA(5) read with section 154 in August 2015.

5.3.5 In Gujarat, CIT-IT & TP Ahmedabad Charge, TPO passed the order of the assessee company (QSG Resource Management Private Limited) under section 92CA(3) for AY 2010-11 in January 2014 at an adjustment of Rs. 2.16 crore. The assessee made a reference before DRP against the upward adjustment. TPO re-computed the average margin of the comparable at 15.43 per cent in pursuance to the DRP’s directions. Since, the margin of assessee was within the permissible limit of five per cent range, no adjustment was proposed and accordingly order under section 143(3) read with section 144C was passed in December 2014 reducing the upward adjustment at Rs. ‘Nil’. Audit scrutiny of TPO order revealed that while giving effect to the direction of DRP order, unadjusted and adjusted margin of one of the comparable (Spry Resources) were taken at 15.52 per cent and 9.42 per cent respectively instead of 33.25 per cent and 21.63 per cent as adopted in order passed under section 92CA(3).As a result, the average adjusted margin of comparables was computed at 15.43 per cent instead of 16.54 per cent. Since the price charged by the assessee falls outside the five per cent limit, an upward adjustment of Rs. 1.00 crore was required to be made under the Act. The Ministry while accepting the audit paragraph has intimated (December 2015) that remedial action is being taken under section 154.

5.3.6 In Gujarat, CIT-IT & TP Ahmedabad Charge, TPO passed the order of the assessee company (KHS Machinery Private Limited) under section 92CA(3) for AY 2011-12 in October 2014 at an adjustment of Rs. 2.27 crore towards royalty charge to AE (KHS Gmbh, Germany). Audit scrutiny of Annual Report of the assessee company revealed that assessee had debited royalty charges of Rs. 3.07 crore in book of accounts towards payment of royalty to the AE. Hence, while determining ALP of royalty transaction, Rs. 3.07 crore should have been taken into account instead of Rs. 2.27 crore as reported by assessee in Form 3CEB. The mistake resulted in short adjustment of Rs. 0.80 crore. The Ministry accepted (December 2015) and has taken remedial action under section 92CA(5) read with section 154 in September 2015.

5.3.7 In Gujarat, CIT-IT & TP Ahmedabad Charge, TPO passed the order of the assessee company (Quintiles Technologies India Private Limited) under section 92CA(3) for AY 2010-11 in January 2014 at an adjustment of Rs. 17.44 crore. TPO rectified the mistake under section 92CA(5) read with section 154 in June 2014 on the representation made by assessee and reduced total upward adjustment to Rs. 1.14 crore from Rs. 6.00 crore on account of interest on advances. Subsequently, on giving effect to DRP’s order, total adjustment of Rs. 8.64 crore which includes Rs. 2.81 crore towards interest on receivables was made under section 144C(5) in January 2015. Audit scrutiny revealed that while passing order under section 92CA(5) read with section 154, assessee’s contention to compute interest on the incremental value of the average amount due for the respective month was accepted by the TPO. Accordingly, adjustment was reduced to Rs. 1.14 crore from Rs. 6.00 crore. However, while giving effect to DRP directions as per section 144C(5), interest was calculated again on the whole of the average amount due for each month for the period from start of the month to the end of the financial year i.e. 31st March 2010. Failure to calculate interest on the incremental value of the average amount due for the respective month resulted in irregular upward adjustment of Rs. 2.27 crore. The Ministry while accepting the audit paragraph has intimated (December 2015) that remedial action is being taken under section 154

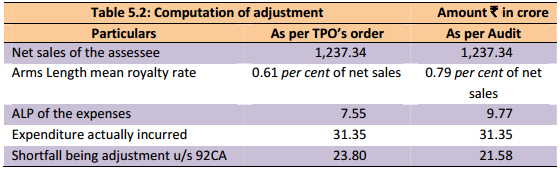

5.3.8 In Gujarat, CIT-IT & TP Ahmedabad Charge, TPO passed the order of the assessee company (Bridgestone India Private Limited) under section 92CA(3) for AY 2011-12 in January 2015 at an adjustment of Rs. 23.80 crore. Audit scrutiny of TPO order revealed that mean margin of sales was worked out at 0.61 per cent on the basis of annual report of FY 2009-10 (relevant to AY 2010-11) instead of 0.79 per cent for AY 2011-12. The mistake resulted in upward adjustment of Rs. 2.23 crore as details given in table 5.2 below.

The Ministry accepted (December 2015) and has taken remedial action under section 154 read with section 92CA(5) in August 2015.

5.3.9 In Andhra Pradesh, CIT-IT & TP Charge, TPO passed the order of the assessee company (Dr. Reddy’s Laboratories Limited) under section 92CA(3) for AY 2011-12 in January 2015 at an adjustment of Rs. 38.92 crore on account of Interest on loans given to AEs, Corporate Guarantee and profit share on marketing and distribution. While computing the shortfall on account of interest charged on loans given to AEs, TPO determined seven per cent as ALP for Interest on loan to AEs and accordingly calculated adjustment of Rs. 7.04 crore wherever the rate of interest on loans granted to AEs was lesser than seven per cent. Audit scrutiny revealed that no adjustment was proposed in respect of loan granted to AE (DRL Australia Private Limited, Australia) as the interest charged (9.74 per cent) by the tax payer was above ALP (seven per cent), however while calculating the adjustment, interest of Rs. 2.69 crore pertaining to said AE was also set-off. The mistake resulted in short adjustment by an equal amount. The Ministry accepted (December 2015) and has taken remedial action under section 92CA(3) read with section 154 in November 2015.

5.3.10 In Andhra Pradesh, CIT-IT & TP Charge, TPO passed the order of the assessee company (Cognizant Technology Services (P) Limited) under section 92CA(3)for AY 2010-11 in January 2014 at an adjustment of Rs. 36.71 crore on account of Interest on ITES services rendered to its AEs. Audit scrutiny revealed that the operating revenue and the operating cost were segregated for AE and non-AE and the adjustment was proposed on AE transactions. The adjusted arm’s length margin for ITES was arrived at 26.23 per cent and the same was marked up to the AE operational cost. However, while arriving at the adjustment, the total operational revenue (AE & non-AE) of Rs. 296.27 crore was deducted from the marked-up AE as against Rs. 290.90 crore relating to AE as detailed in table 5.3 below.

The Ministry accepted (December 2015) and has taken remedial action under section 92CA(3) read with section 154 in November 2015.